Most of the world’s oil is turned into a handful of main petroleum products: motor gasoline, diesel/gasoil, jet fuel/kerosene, marine and heavy fuel oils, LPG and other light gases, naphtha and petrochemical feedstocks, plus non-fuel products such as bitumen/asphalt, lubricants, waxes and solvents. Together, they power transport, industry, buildings and global supply chains.

Petroleum products are simply what you get when crude oil is refined, blended and sometimes further processed. They differ by boiling range, composition and specification — but from a business perspective, they boil down to: fuels, feedstocks and specialties that move people, move goods, and make materials.

In practice, almost every refinery slate is dominated by:

Road fuels: gasoline, diesel and gasoil

Aviation fuels: jet fuel and kerosene

Marine fuels: very-low-sulfur fuel oil (VLSFO) and marine gasoil

Light gases: LPG and other natural gas liquids (NGLs)

Petrochemical feedstocks: naphtha, LPG/ethane

Non-fuel products: Bitumen, lubricants, waxes, solvents and petroleum coke

Highlights & Key Sections

What are the main petroleum products?

Across most regions, the main petroleum products are those with the highest and most stable demand: road fuels, aviation fuels, marine fuels and petrochemical feedstocks. Transport fuels supply roughly half of global oil demand, while chemical feedstocks account for about one sixth and are still growing.

Snapshot table: key product families at a glance

| Product family | Typical role | Key buyers/users | Example applications |

|---|---|---|---|

| Motor gasoline | Primary light-duty road fuel | Fuel retailers, fleets, governments | Cars, motorcycles, small engines |

| Diesel & gasoil | Heavy-duty transport & industrial fuel | Trucking fleets, logistics, mines, farms | Trucks, buses, rail, construction, generators |

| Jet fuel & kerosene | Aviation & some heating/lighting | Airlines, airports, defense | Commercial flights, cargo planes, remote heating |

| Marine fuels & fuel oil | Shipping & large engines | Shipowners, ports, utilities | Ocean tankers, bulk carriers, some power plants |

| LPG & light NGLs | Heating, cooking, feedstock | Gas distributors, traders, petrochemical plants | Bottled gas, petrochemical crackers |

| Naphtha & feedstocks | Petrochemical building blocks | Steam cracker operators, chemical makers | Plastics, synthetic fibers, solvents |

| Bitumen/asphalt | Construction binder | Road contractors, infrastructure firms | Road paving, roofing membranes |

| Lubricants & specialties | Equipment protection, consumer goods | OEMs, distributors, industrial users | Engine oils, greases, waxes, solvents |

Below, we break each group down in practical, business-focused terms.

1. Motor gasoline – still the king of light-duty transport

Gasoline is a light, volatile fuel designed for spark-ignition engines. It’s blended to precise specs (octane rating, vapor pressure, sulfur, oxygenates) so cars start easily, run smoothly and meet emissions standards.

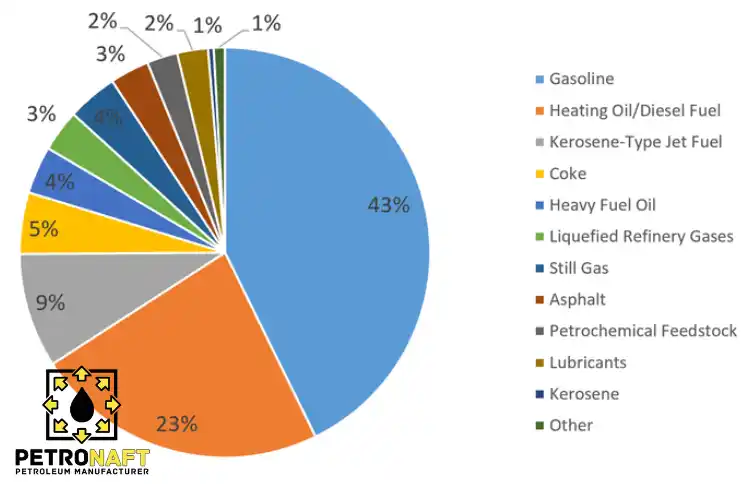

In mature markets like the United States, gasoline alone has accounted for about 40–45% of total petroleum product consumption, far more than any other single product.

Where gasoline dominates

Passenger car fleets (especially in North America, parts of Asia and the Middle East)

Motorcycles and scooters in dense urban markets

Small equipment like generators, lawn tools, pumps

Key specs buyers watch

Octane (RON/AKI): Determines resistance to engine knock

Sulfur content: Ultra-low sulfur gasoline is now standard in most OECD markets

Reid Vapor Pressure (RVP): Controls volatility for seasonal and climate conditions

Bio-component content: Ethanol or other oxygenates affect energy content and compatibility

Trend to watch

Electric vehicles and efficiency standards are flattening gasoline demand in many advanced economies, while emerging markets still grow from a lower motorization base. Forecasts to 2030 show overall oil demand growth slowing sharply as EVs and fuel economy standards bite, even though total oil consumption hasn’t yet peaked in many scenarios.

2. Diesel and gasoil – the workhorses of heavy transport and industry

“Distillate fuel oil” covers several products, but diesel and heating oil/gasoil are the most important. They run compression-ignition engines and industrial burners, prized for high energy density and efficiency.

In the US, distillate fuels consistently represent around one fifth of total petroleum consumption, making diesel the second-largest product after gasoline. Globally, diesel is critical for freight, agriculture and construction, and is also one of the biggest exported petroleum products.

Major uses

Long-haul trucking and local delivery fleets

Buses, coaches and some rail systems

Agricultural machinery, construction equipment, mining trucks

Standby and off-grid generators

Heating oil in colder-climate buildings

Key diesel parameters for buyers

Cetane number: Higher cetane generally improves cold starts and combustion smoothness

Sulfur level: Ultra-low-sulfur diesel (ULSD) is vital for modern engines and after-treatment systems

Cold flow properties (CFPP/pour point): Critical in cold climates to avoid waxing

Biofuel blend (B5, B7, B20): Affects emissions, storage stability and OEM warranties

Market trend

Road diesel demand is showing structural decline in some major markets due to more efficient engines, logistics optimization and gradual electrification. At the same time, diesel remains vital in emerging economies and as an export-oriented product for complex refineries.

Mini case example

A regional logistics fleet switched to a higher-cetane ULSD and tightened preventive maintenance (fuel filtration, injector cleaning). Combined with route optimization, they cut fuel burn by 3–5% and reduced unplanned downtime — a small change in product and practice, big impact on cost per ton-kilometer.

3. Jet fuel and kerosene – aviation’s lifeblood

Jet fuel (Jet A/Jet A-1) is a middle distillate similar to kerosene but formulated for aviation: tight freezing-point, thermal stability and cleanliness requirements.

Uses

Commercial passenger and cargo aircraft

Business jets and some military aircraft

Kerosene (non-aviation) for heating or lighting in certain regions

Why jet fuel matters now

Since air travel rebounded from pandemic lows, jet fuel has been one of the fastest-growing refined products, driving a significant share of recent oil-demand growth.

Sustainable aviation fuel (SAF)

Many airlines now co-burn SAF (from bio-based or synthetic sources) blended into conventional jet fuel. For buyers and airports, this introduces new considerations:

Contractual guarantees on blend ratios

Compatibility with aircraft and fuel systems

Certification under schemes like CORSIA or national mandates

For investors and suppliers, jet fuel is one of the few major products with clear growth headroom even under aggressive decarbonization scenarios.

4. Marine fuels and heavy fuel oil – powering global shipping

Marine fuels range from cleaner marine gasoil (MGO) to heavier residual blends known as fuel oil. Shipping has historically consumed a large share of high-sulfur fuel oil, but regulation has reshaped the mix.

Core segments

VLSFO (Very-Low-Sulfur Fuel Oil): Blended to meet IMO 2020 sulfur limits for most ocean-going vessels

MGO/MDO: Lighter, cleaner distillate fuels used near coasts, in emission control areas, and for some engines

HSFO with scrubbers: Still used where ships have exhaust cleaning systems

Buyer priorities

Sulfur compliance with international and local rules

Viscosity and stability for engine performance

On-spec density and energy content for voyage planning

Reliable supply at key bunkering hubs (Singapore, Rotterdam, Fujairah, etc.)

Transition signals

Shipowners increasingly test LNG, methanol, biofuels and, in the longer term, ammonia as alternative marine fuels. For now, however, refined petroleum products remain the backbone of ocean transport.

5. LPG and other light gases – from cooking stoves to crackers

Liquefied petroleum gas (LPG) is mainly propane and butane, stored and transported as a pressurized liquid. Other light natural gas liquids (NGLs) include ethane, which is crucial for petrochemicals.

Key uses

Residential: Clean cooking and heating, especially where pipelines are limited

Commercial/industrial: Space heating, small boilers, process fuel

Chemical feedstock: Propane, butane and ethane cracked into olefins for plastics

In many developing countries, LPG adoption has been a major public-health measure, replacing traditional biomass and kerosene. At the same time, in large petrochemical hubs, LPG and ethane demand is rising as feedstocks, supporting the growth of plastics and synthetic materials.

What LPG buyers focus on

Propane vs butane ratio (affects vapor pressure and performance)

Cylinder quality and safety standards

Storage and logistics capabilities at terminals and depots

Price linkage to key international benchmarks

6. Naphtha and petrochemical feedstocks – the hidden giants

Naphtha is a light to medium distillate fraction used mainly as a steam cracker feedstock. Along with LPG/ethane, it is a primary input for:

Ethylene and propylene

Aromatics (benzene, toluene, xylenes)

Downstream plastics, fibers, solvents and resins

Petrochemical feedstocks already account for roughly 16% of global oil demand, with their share expected to rise to about one barrel in six by 2030, even as total oil use slows.

Trends reshaping naphtha markets

Capacity overbuild: New crackers in Asia and the Middle East have created periods of oversupply and pressure on margins.

Competing feeds: Ethane- and LPG-based crackers offer cost advantages in some regions.

Energy transition: Even in scenarios with plateauing oil demand, petrochemicals remain one of the last-growing segments.

Practical checklist for naphtha buyers

Paraffinic vs naphthenic/aromatic content (impacts ethylene yield)

Sulfur, nitrogen and metal contamination

Distillation range and vapor pressure

Contract structure (CFR vs FOB, term vs spot, linkage to crude or naphtha benchmarks)

7. Bitumen/asphalt – infrastructure’s glue

Bitumen (asphalt) is the heavy, viscous residue from atmospheric and vacuum distillation or from further processing of residue. It acts as a binding material for aggregates in roadbuilding and as a waterproofing layer in construction.

Main uses

Road and highway surfaces

Airport runways and ports

Roofing shingles and membranes

Waterproofing for foundations and civil structures

Demand is heavily tied to infrastructure and construction spending. For example, during periods of intense road-building activity, national bitumen consumption can spike dramatically — one recent instance saw bitumen demand in a major Asian market jump nearly 30% year-on-year.

What bitumen buyers evaluate

Penetration grade or performance grade (PG) vs climate and axle loads

Softening point and viscosity

Polymer modification for rutting and cracking resistance

Storage stability and handling temperature

8. Lubricants, waxes, solvents and other specialties

While smaller by volume, specialty petroleum products are critical for equipment reliability and many consumer goods.

Lubricants and base oils

Engine oils for on-road and off-road vehicles

Industrial lubricants for turbines, compressors, hydraulic systems

Metalworking fluids and greases

Specialty products

Paraffin waxes: Candles, packaging, board products, hot-melt adhesives

Solvents: Paints, coatings, cleaning agents, adhesives

Petroleum coke: Fuel in cement and power plants, some industrial processes

For industrial buyers, lubricant selection can materially affect energy consumption, component life and maintenance cycles, making these products strategically important despite their modest share of total barrels.

Energy vs non-energy uses: how barrels are actually used

Crude oil gets split between energy (fuels and combustion) and non-energy uses (materials and feedstocks).

Approximate high-level split:

Energy uses (~80%): Gasoline, diesel, jet fuel, marine fuels, heating oil, LPG used as fuel

Non-energy uses (~20%): Naphtha, LPG/ethane, lubricants, bitumen, waxes and other feedstocks that become plastics, chemicals and materials

For business planning, this matters because:

Energy uses are more exposed to fuel-efficiency regulations, electrification and carbon pricing.

Non-energy uses are more exposed to plastics policy, recycling mandates and circular-economy trends.

When you analyze the main petroleum products, look not just at volume but at which side of this energy/non-energy divide they sit on.

How the main petroleum products are changing: three big trends

1. Slowing growth in road fuels

Tightened efficiency standards, better logistics and rising EV penetration are flattening or reducing gasoline and diesel demand in many advanced economies.

New oil market outlooks show global demand still rising short term, but growth rates shrinking and a plateau in the 2030s increasingly likely.

2. Petrochemicals and jet fuel as demand drivers

Petrochemical feedstocks (naphtha, LPG/ethane) are set to remain a major growth driver for oil, accounting for an increasing share of total barrels consumed.

Jet fuel demand recovered strongly after the pandemic and has contributed disproportionately to recent oil-demand growth, especially in markets where air travel has rebounded fastest.

3. Decarbonization pressure across the barrel

Regulations push sulfur and emissions lower for fuels, reshaping marine and road products.

Many countries are rolling out blending mandates (biofuels, SAF), fuel CO₂ standards and carbon pricing.

Future growth potential differs dramatically by product: aviation and petrochemicals look resilient; conventional gasoline and diesel face the steepest policy headwinds.

For investors, traders and industrial buyers, this means not all products carry the same long-term risk even if they originate from the same barrel.

Practical buyer’s guide: mapping needs to products

If you’re deciding which petroleum product and grade best fits your application, structure the decision around four questions:

What is the primary function?

Moving people or goods → gasoline, diesel, jet, marine fuels

Producing heat/power → gasoil, fuel oil, LPG

Making materials → naphtha, LPG/ethane, specialty feeds

Protecting equipment → lubricants

What are the critical technical constraints?

Engine type and OEM approvals

Emission limits and sulfur caps

Climate (cold flow, volatility, oxidation stability)

Process yields in chemical plants

What are your regulatory and ESG obligations?

Need for ULSD, IMO-compliant bunkers, SAF blends, biofuel blends

Carbon and air-quality limits in your jurisdiction

Corporate climate or circularity targets

What are your commercial priorities?

Price stability vs spot exposure

Supply security (multiple grades, storage, logistics)

Long-term indexation (to crude benchmarks, product indices or formula pricing)

Use these questions to narrow down which of the main petroleum products truly fits your technical and strategic needs, then go deeper on specifications and supplier capability.

Executive summary & practical checklist

Executive summary

The main petroleum products are concentrated in a few high-volume categories: road fuels (gasoline, diesel), jet fuel, marine fuels, LPG/light gases, petrochemical feedstocks (naphtha, LPG/ethane) and non-energy products such as bitumen, lubricants and waxes.

Transport fuels still dominate volumes, but petrochemicals and aviation increasingly drive growth as efficiency and electrification cap gasoline and diesel.

For businesses, the key is matching product type and grade to engine/process requirements, regulatory constraints and long-term decarbonization strategy.

Quick checklist for professionals and buyers

Before you sign your next supply contract, confirm:

✅ Correct product family (fuel vs feedstock vs specialty) for your application

✅ Compliance with all relevant specs (sulfur, octane/cetane, viscosity, cold flow, volatility, flash point)

✅ Regulatory fit: emissions, blending mandates, sustainability or origin documentation

✅ Infrastructure readiness: storage, handling equipment, safety systems and quality control procedures

✅ Commercial robustness: pricing formula, credit terms, alternative supply options and contingency plans

If each box is ticked, you’re far more likely to get the right barrel, at the right quality, on the right terms.

FAQ: main petroleum products and their uses

1. Which petroleum product is used most worldwide?

In many large markets, motor gasoline has historically been the single biggest product by volume, especially where car ownership is high. However, when you combine diesel, jet fuel and marine fuels, transport middle distillates as a group rival or exceed gasoline’s share of total demand.

2. What is the difference between crude oil and petroleum products?

Crude oil is the unprocessed mixture of hydrocarbons pumped from reservoirs. Petroleum products are the refined outputs — gasoline, diesel, jet fuel, LPG, naphtha, bitumen, lubricants and others — each tailored via distillation, cracking, reforming and blending to meet specific performance and regulatory requirements.

3. How are petrochemical feedstocks different from fuels?

Fuels are burned to release energy, so their value lies in combustion properties and emissions. Petrochemical feedstocks like naphtha and LPG/ethane are not usually burned; they are converted into building-block molecules (ethylene, propylene, aromatics) that become plastics, fibers and other materials, making yield and purity the key value drivers.

4. Are the main petroleum products likely to be replaced soon?

Some uses will shrink or switch fuels — for example, gasoline in passenger cars — but others, notably jet fuel and petrochemical feedstocks, are more difficult to decarbonize and remain resilient in most energy scenarios. Alternative fuels, electrification and efficiency will change the mix rather than eliminate petroleum products overnight.

5. What quality documents should I request when buying petroleum products?

Professionals typically ask for a recent certificate of quality (CoQ) or laboratory test results against agreed specifications, plus relevant standards (ASTM, EN, ISO), safety data sheets and, where applicable, proof of compliance with environmental or blending regulations. For long-term deals, independent inspection reports at loading and discharge are also common practice.

Sources

International energy statistics and analysis on global oil demand, product categories and sectoral use.

International Energy Agency – Oil and oil products data and reportsComprehensive data and explanations on petroleum products, refining processes and product consumption by type.

U.S. Energy Information Administration – Oil and petroleum products explainedGlobal statistical data on energy markets, including oil demand by product and region.

Energy Institute – Statistical Review of World EnergyMedium- and long-term outlooks for refined product demand, petrochemical and jet fuel trends and the impact of the energy transition on oil.

International Energy Agency – Oil market and outlook reports